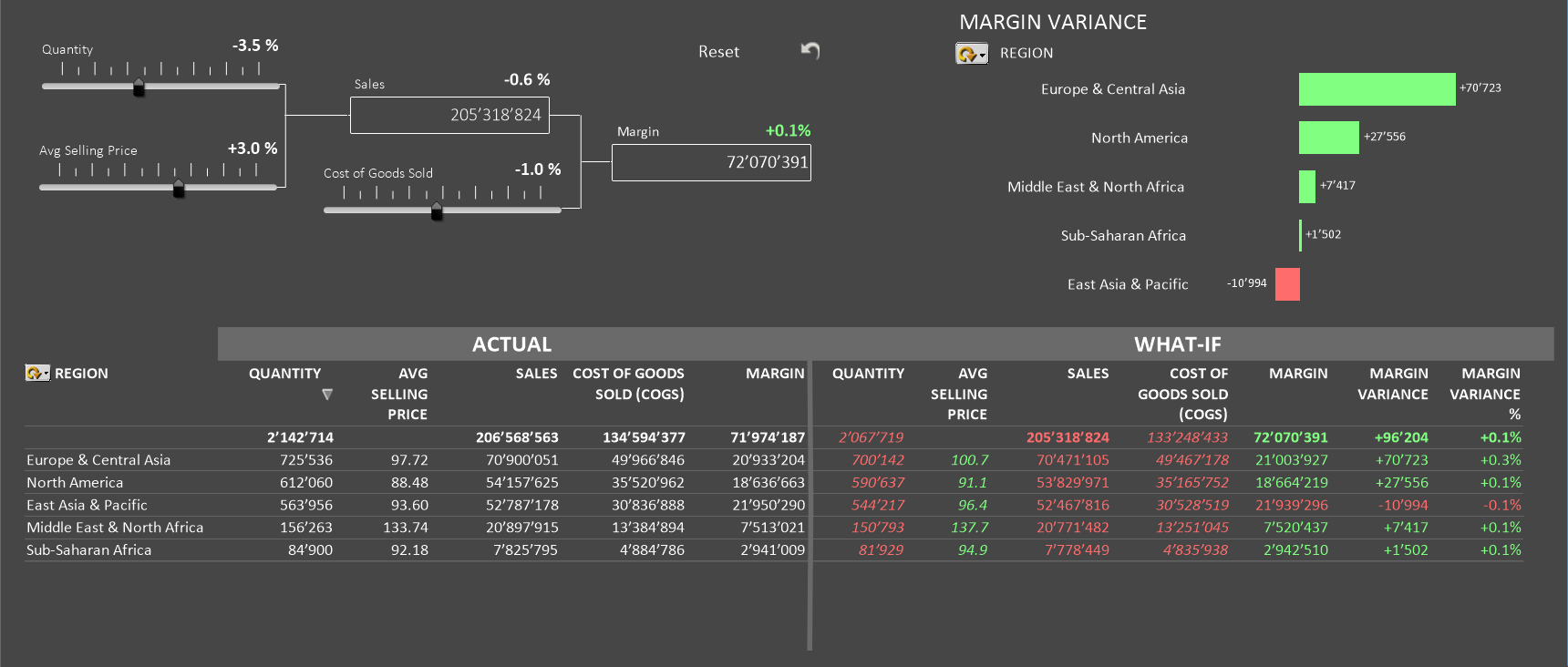

Intuitive What-If Scenario Testing

Applications

Simulation is one of the most widely used quantitative methods because it is so flexible and can yield so many useful results. Here's just a sample of the applications where simulation is used:

□ Choosing drilling projects for oil and natural gas

□ Evaluating environmental impacts of a new highway or industrial plant

□ Setting stock levels to meet fluctuating demand at retail stores

□ Forecasting sales and production requirements for a new drug

□ Planning aircraft sorties and ship movements in the military

□ Planning for retirement, given expenses and investment performance

□ Deciding on reservations and overbooking policies for an airline

□ Selecting projects with uncertain payoffs in capital budgeting

□ Evaluating environmental impacts of a new highway or industrial plant

□ Setting stock levels to meet fluctuating demand at retail stores

□ Forecasting sales and production requirements for a new drug

□ Planning aircraft sorties and ship movements in the military

□ Planning for retirement, given expenses and investment performance

□ Deciding on reservations and overbooking policies for an airline

□ Selecting projects with uncertain payoffs in capital budgeting

Models

In a simulation, we perform experiments on a model of the real system, rather than the real system itself. We do this because it is faster, cheaper, or safer to perform experiments on the model. While simulations can be performed using physical models such as a scale model of an airplane our focus here is on simulations carried out on a computer.

Computer simulations use a mathematical model of the real system. In such a model we use variables to represent key numerical measures of the inputs and outputs of the system, and we use formulas, programming statements, or other means to express mathematical relationships between the inputs and outputs. When the simulation deals with uncertainty, the model will include uncertain variables whose values are not under our control as well as decision variables or parameters that we can control. The uncertain variables are represented by random number generators that return sample values from a representative distribution of possible values for each uncertain element in each experimental trial or replication of the model. A simulation run includes many hundreds or thousands of trials.

Our simulation model will calculate the impact of the uncertain variables and the decisions we make on outcomes that we care about, such as profit and loss, investment returns, environmental consequences, and the like. As part of our model design, we must choose how numerical values for the uncertain variables will be sampled on each trial.

Monte Carlo

Monte Carlo simulation named after the city in Monaco famed for its casinos and games of chance is a powerful method for studying the behavior of a system, as expressed in a mathematical model on a computer. As the name implies, Monte Carlo methods rely on random sampling of values for uncertain variables, that are "plugged into" the simulation model and used to calculate outcomes of interest. With the aid of cloud computation, we can obtain statistics and view charts and graphs of the results.

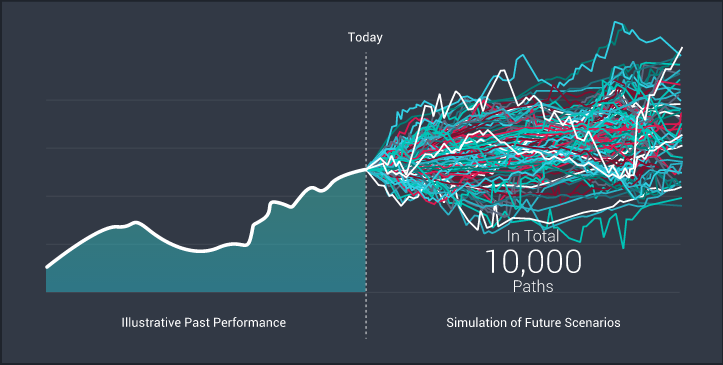

Monte Carlo Simulation Models 10,000 Potential Paths of a KPI

Monte Carlo simulation is especially helpful when there are several different sources of uncertainty that interact to produce an outcome. For example, if we're dealing with uncertain market demand, competitors' pricing, and variable production and raw materials costs at the same time, it can be very difficult to estimate the impacts of these factors in combination on Net Profit. Monte Carlo simulation can quickly analyze thousands of 'what-if' scenarios, often yielding surprising insights into what can go right, what can go wrong, and what we can do about it.